AI data centers run into grid reality: power hookups and utility capacity move to the center of the trade

A source bundle tying AI product headlines to data-center infrastructure highlights a growing bottleneck: electricity supply, grid interconnections and local scrutiny. Markets are watching how power limits shape cloud expansion, chip demand and utilities’ load-growth outlook.

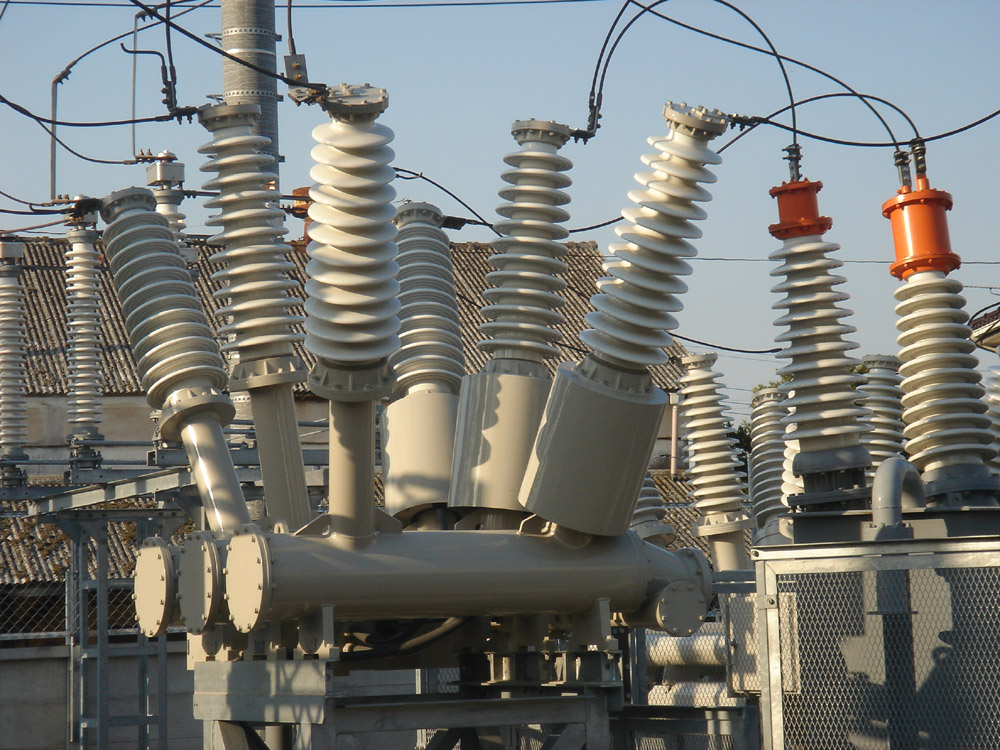

The AI buildout is keeping Wall Street’s attention on a less glamorous constraint: where the electricity will come from, and how fast new data centers can actually connect to the grid.

A bundled set of AI product and infrastructure headlines highlighted by an AI infrastructure and local-permitting source package links surging cloud spending and data-center demand with power constraints, grid strain, water usage, and local permitting scrutiny. The same bundle flags community protests and demonstrations as a practical risk factor that can slow, delay or, in some cases, push developers to rethink projects—without making any single outcome certain.

The immediate market read-through runs in two directions at once. On one side are the companies selling the picks-and-shovels of AI compute, including chipmakers such as Nvidia (NVDA) and the broader tech complex represented by the Nasdaq-100 (QQQ). On the other side are utilities (XLU) and grid-related infrastructure, where rising data-center load can be a demand tailwind—but also a source of regulatory and political friction when the question shifts to who pays for upgrades.

The source bundle frames the AI cycle as an end-to-end supply chain problem: cloud providers and large platforms such as Microsoft (MSFT), Alphabet (GOOGL), Amazon (AMZN) and Meta (META) are pushing capacity additions to meet AI service demand, which supports advanced chips and data-center equipment. But electricity availability and interconnection timing can become gating factors that determine when new capacity is usable, not just when it is announced or started.

Water use and siting issues add another layer. The same package ties large buildouts to water consumption concerns, with permitting scrutiny and public resource tension showing up in local hearings and community responses. For investors, those frictions matter because they can influence construction schedules, operating costs, and the reliability of growth assumptions tied to data-center expansion.

{kind=link}

OmniMint interpretation: the market’s AI conversation is broadening from “who has the best model?” to “who can secure the physical inputs”—power, land, and water—fast enough to keep AI services scaling. That shift does not automatically reduce AI demand, but it can change its timing and geography, and it can redistribute value across the stack. If grid bottlenecks lengthen deployment timelines, the industry may see more emphasis on utilization of existing capacity, power procurement strategies, and buildout pacing.

For big cloud and platform names, power constraints are a double-edged story. They can limit near-term expansion in certain regions, but they can also raise the strategic value of secured capacity and successfully permitted sites. For NVDA and other AI hardware beneficiaries, the same constraints can introduce more variability into the cadence of deliveries and installations, even if longer-term demand remains supported by continued infrastructure expansion.

Utilities sit at the center of the tension. Data centers represent large, often concentrated load growth—supportive for electricity sales and grid investment—but they also raise questions about transmission buildouts, system reliability, and the allocation of upgrade costs across customers. The permitting and community-pushback element flagged in the source bundle also applies to grid expansions themselves, which can face their own delays.

What comes next is likely to be driven by a mix of operational and political signals: how quickly interconnections progress, whether local authorities tighten review of power and water impacts, and whether community opposition becomes a recurring source of delay risk. Markets will also keep tracking how cloud providers frame infrastructure plans alongside AI product launches, since the ability to deliver compute at scale increasingly depends on navigating these real-world constraints.

In short, AI may be software-driven at the user level, but the next phase of the trade is increasingly tied to grid realities—and that keeps both megacap tech and utilities in focus.

OmniMint uses outside reporting as citation anchors, then adds original market context and workflow analysis from published research data.

- AI buildout keeps stocks, cloud demand, power, water, and local pushback in focus AI infrastructure / local permitting source bundle - 2026-05-25T14:00:00Z

Source attribution: AI infrastructure / local permitting source bundle. Source attribution is preserved; this page is published as an OmniMint read.